![[National Homeownership Month] How Your Side Hustle, Crowdfunding, & Airbnb, Can Make You A Homeowner!](https://images.squarespace-cdn.com/content/v1/6011ce08663bad3a50903423/1622583282319-ZU94QNT9NFO2718P72RH/homeownership.jpg)

[National Homeownership Month] How Your Side Hustle, Crowdfunding, & Airbnb, Can Make You A Homeowner!

New Ways To Become A Homeowner In the New Economy

By: Stacey Tisdale

Homeownership in the United States soared to its highest level in 12 years in 2020, as low mortgage rates and the coronavirus pandemic prompted more Americans to want to own a home. The biggest group of new homebuyers were those under the age of 35. The homeownership rate among Black Americans increased to 47%, the highest since 2008, whereas just a year prior, Black homeowners had fallen to its lowest rate on record, according to the U.S. Census Bureau.

Challenges still face potential homeowners when qualifying for a mortgage, especially among the self-employed, as more and more Americans turn to the gig economy, relying on income from things like side hustles and freelance work. A survey by FlexJobs found that 36% of American workers have been freelancing during the pandemic – that’s an increase of 2 million freelancers from 2019. And more than a third are freelancing full-time.

[Click HERE to get our free, Weekly Wealth Builder Newsletter]

By 2027, the gig workers, which includes temp workers, independent contractors, and freelancers, will be the majority of the work force, and they want to own homes. In a survey done by Fannie Mae, 75% of gig workers want to buy a home at some point, yet 69% don’t see it happening in their next move, acknowledging that the majority of lending practices are one size fits all, requiring a steady paycheck, a W-2, and a good credit score, things that don’t exist for many gig workers.

New Solutions for the Gig Economy

The good news is that new initiatives and mortgage products can help would-be homeowners realize their dreams, considering factors like side hustle income, and offering options like crowdfunding for down payments.

“Our primary job is to provide lenders the cash they need to provide safe products like the 30-year fixed mortgage available to everyone, at a reasonable rate,” says Fannie Mae VP Danielle McCoy.

Crowdfunding & Homeownership?

Fannie Mae has joined forces with mortgage-banking firm CMG Financial. CMG works with housing advocates, agencies, and secondary lenders like Fannie Mae, to find solutions for the borrower who might not have all the income or cash to buy a home. CMG and Fannie Mae created HomeFundIt.com, the first and only crowdsourcing platform for the sole purpose of raising cash for a down payment and closing costs. A prospective buyer publishes their story online with the hope that family and friends will be moved to donate enough cash to cover these costs.

HomeFundIt also offers $1,500 closing cost grants and feature called UpIt raises funds when the borrower, family, and friends shop online. Companies like the Gap, Walgreens and Overstock.com give a percentage of the sale, company determined, to the home buyer’s fund. All funds are strictly for down payments and closing costs.

Paul Akinmade, the chief Marketing Officer at CMG remembers, “When I worked as a banker for a mortgage bank, I had to reject people for a mortgage, but when I explained why and what they needed to do to be approved, I would help them find a way to become homeowners.”

“In the 20 months since Homefundit.com launched, more than 550 campaigns have been funded,” he adds.

[Click HERE to learn about The Investing Habits of Wealth Blacks]

New Solutions for a New Economy

Fannie Mae also has a product called “Home Ready.” It’s targeted towards low to moderate income borrowers who want to buy, but have limited cash for a down payment, up to a 50% debt-to-income ratio, and a FICO score as low as 620. Side gig rental income is considered, and parents can be co-borrowers.

In addition, the borrower makes down payment of just 3%, which can be funded multiple ways, including crowdfunding or mortgage insurance that can be cancelled once equity reaches 20%.

Fannie Mae and Freddie Mac have launched new technology that analyzes all the info a freelancer must submit – years of tax returns with all the backup information – in minutes not days, when it was done manually. This saves so much time and keeps the costs down for the borrower.

A Dream Can Become Reality

71% of lenders allowed borrowers use gig income to secure a mortgage and 89% of lenders expect this number to grow. With new options like HomeFundIt.com and Home Ready, dreams can become reality.

To take advantage of these new options, you must first determine if your lender is backed by Fannie Mae and offers these products, and as McCoy says, “You must do as much research about your mortgage as you do about your home before starting the homebuying process.”

![[Diversity & Inclusion] How Workplace Bias Damages Asian Women's Lives](https://images.squarespace-cdn.com/content/v1/6011ce08663bad3a50903423/1622038151510-9BA62UJYWT6QCSGE832N/b2wHqOHXm1xyihtFi8zKd07sShYyEJof.jpg)

[Diversity & Inclusion] How Workplace Bias Damages Asian Women's Lives

When The ‘Model Minority’ Crashes Into The ‘Bamboo Ceiling’

By: Stacey Tisdale

Asian American women are most likely to have graduate degrees--but least likely to be in upper management. It's called the Bamboo Ceiling and it often leads to physical and psychological problems, like depression, stress, and increased suicide attempts, especially among young Asian American women. The impact of microaggressions and workplace bias also cause women of color to leave their careers rather than try to "fit in" to a corporate culture that doesn't accept them as they are.

Wealth Wednesdays is exposing the impact of workplace discrimination on the lives and careers of women of color in a new series we're calling Very Courageous Conversations, with our partners at Paradigm for Parity, an organization whose goal is gender and racial equity in corporate leadership. It's a brutally honest but also inspiring discussion, hosted by Wealth Wednesdays' Stacey Tisdale.

![[Personal Finance] What Wealthy Blacks Can Teach Us About Investing](https://images.squarespace-cdn.com/content/v1/6011ce08663bad3a50903423/1621455696201-MXG1LSQ8DABPJM9B1PI9/Wealthy+Blacks.jpg)

[Personal Finance] What Wealthy Blacks Can Teach Us About Investing

An Intimate Look At How Race & Culture Influence Our Investment Choices

By: Stacey Tisdale

It’s important to consider the historic aspect of the place homeownership holds in Black culture. Owning land is what many of our forefathers experienced as the only way to gain wealth, conditioning many of their children to believe the same.

While experience and evolution have breathed space around those deep-seated beliefs – Black millennials are entering the stock market at a higher rate than any other group in the United States – changing attitudes about where to park wealth is a challenge for many.

The Investing Habits of Wealthy Blacks

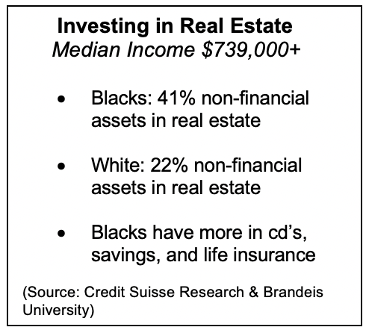

Wealthy Blacks and Real Estate

Even when it comes to investments other than their primary home, affluent Blacks have tended to move towards real estate.

Those with a median income of $739,000 or more invest 41 percent of their non-financial assets in real estate, compared to just 22 percent of Whites in the same income bracket.

The researchers who conducted the study concluded that this more conservative approach of the top 5% of African Americans to investing is understandable when looking at the constrained social mobility trends of the community, and the lower levels of overall economic security.

Socioeconomic disadvantages like predatory lending practices and other historic events have left some Blacks distrustful of the financial services industry.

In addition, many Blacks who fall in the top wealth categories are the first generation of wealth – which may also lead to a cautious approach to investing.

[Are Your Early Lessons About Money Hurting You Now? Read THIS to Find Out]

Lessons Learned

The 2008 financial crisis was a financial disaster for many Americans – particularly those in the Black community - because the vast majority had their net worth locked up in their primary residence.

Analysts say that’s one of the reasons we are seeing more Blacks, particularly millennials and Gen Z, diversify their investment holdings into assets like stocks. Case in point, Black Americans invested in the stock market 3 times more than white Americans last year, according to an Ariel Investment and Charles Schwab survey.

In addition, 70 percent of Black millennials under the age of 40, earning at least $50,000 a year invest in stocks.

[ Angela Yee, On The Importance of Knowing Your Worth. Click HERE.]

What Happens to Wealthy Black Men

Blacks experience affluence, and its financial benefits differently than other groups, particularly Black men.

Researchers at Stanford & Harvard Universities, working with the Census Bureau, conducted a sweeping study that traced the lives of millions of children and found that Black Boys raised in America, even in the wealthiest families, earn less in adulthood than White boys with similar backgrounds

Researchers concluded that if this inequality cannot be explained by individual or household traits, much of what matters probably lies outside the home — in surrounding neighborhoods, in the economy and in a society that views black boys differently from White boys, and even from black girls – as Black women do not experience this same dynamic.

Some of the researchers even went so far as to say that what happens to these affluent Black boys and men is the major cause of the wealth gap.

[Click HERE to get our free, Weekly Wealth Builder Newsletter]

Building Wealth

These socioeconomic tragedies make investing even more imperative for the Black community. The financial markets can help us empower ourselves and level our own economic playing fields.

The world is changing in every way. Political and economic structures are changing. Long-standing racial, religious, and gender stereotypes are being disrupted. This is forcing many of us to take a long, hard look inside, and take personal responsibility for patterns that no longer serve our well-being.

Money’s greatest gift is that it can reflect back to us where we are not using our resources in ways that reflect our highest ideals and values.

Wealth Wednesdays Co-Host, Angela Yee, Shares The Importance of Knowing Your Worth

By: Stacey Tisdale

Angela Yee is a force to be reckoned with, a powerful success in radio, in business and in life. Yee has come a long way from her roots in East Flatbush, Brooklyn. She attributes her rise and ability to thrive in an industry run and populated almost exclusively by men to hard work and knowing her self-worth. One of the co-hosts of the popular morning radio show, The Breakfast Club, on NYC’s highly rated Power 105.1, Yee never imagined she’d be such a success, and have the things she has today, like a house.

“As far as I can remember, starting in kindergarten, I wanted to be a writer. I went to Wesleyan University and majored in English,” Yee says, “but I also grew up as a music lover and I would listen to the radio with headphones on for hours at a time. I even got turntables and DJ’ed for a couple of years when I got out of college.”

Perseverance Pays Off

A summer internship at Wu-Tang Management led to a full-time position for Yee. She became the assistant to the CEO. And just like that, Yee’s chosen career path changed completely. At 21, Yee oversaw payroll, attended meetings at other record companies with her boss, and put together benefits, like a free fair that offered health information, rides and a concert. Yee’s mother, who often worked seven days a week, was her inspiration for working so hard.

“I was always the first one in and the last one to leave. Every time my boss called, I was there. He told me when I’m not in the office, you’re me. I loved the job and networked non-stop. It’s so important to go to events, meet the people you’re talking to on the phone. Show support, don’t just hang with your friends put yourself out there” Yee says.

The hard work – and the networking — paid off. When Yee learned Eminem would have his own channel on Sirius radio, Yee called Eminem’s manager to see if she could get an “introduction” from him with Sirius – for a job in marketing maybe. Yee had met Eminem’s manager when she helped launch the Shady Limited Clothing Line. To her surprise, he mentioned an opening for an on- air talent in one of the new shows and suggested Yee audition for the job. Yee had found her calling.

Taking it To the Next Level

After six successful years with Sirius, and two of her own shows on the air, Yee walked away, for a job at Power 105.1, a local NYC radio station. Yee felt under-appreciated by the men, and only men, in leadership at Sirius. They weren’t treating her fairly or respecting hip hop.

“They thought they made me, but it was my hard work that made things happen. I had offers over the years so I knew I’d be ok, but leaving Sirius was scary nonetheless. All I can say is, if you feel like it’s not working out for you, then you have to be really great at what you do, know your self-worth, and have great relationships so at the end of the day, if you have to walk away you can” says Yee.

Things weren’t always as easy as it might seem for Yee. She got into serious debt in college when she maxed out several credit cards and stopped paying any of the bills. Yee spent years paying off the debt and rebuilding her credit only to run into trouble again when she was managing a new rapper and maxed her credit card again. That was the last time. Today, Yee checks her bank account every day, she pays off her credit cards in full every month and she invests. She owns a home and a juice bar/hang out spot in Brooklyn and three houses in Detroit.“

Yee, newly inducted into the Radio Hall of Fame with co-hosts DJ Envy and Charlamagne tha God, also is the host of “Established with Angela Yee,” a new celebrity interview series streaming on Fox Soul. Yee previously worked with Fox Soul, hosting the four-part limited series “Motown Countdown with iHeartRadio’s Angela Yee.” Her new focuses on pivotal career moments and milestones of the interviewee.

Yee says, “So much of being successful is about building relationships, true relationships. Treat everybody equally, know people’s names, show them you care. I’m a good person, I want to do well, but I want others to do well too. I like to make money, but I like to use it to help people. I believe If you put out great vibes, you will get back great vibes.”

Low on Confidence? Start Saving & Investing Money

Study Finds That Saving & Investing Builds Confidence

A study by TIAA finds that Americans are having a bit of a crisis of confidence when it comes to their financial security, with fear of events like an unexpected expense, financially supporting loved ones, or even cuts to Social Security and Medicare impacting their peace of mind.

“A major lesson of this survey is that

effectively addressing uncertainties is key to feeling financially secure.”

– Lori Dickerson Fouché, CEO, TIAA Financial Solutions

The Cost of Financial Stress

While many people can relate to the issues TIAA found to be factors in causing financial stress, few understand the impact that stress has on overall well-being.

People with financial stress are more than twice as likely to experience mental health problems, including depression and anxiety.

29% of people with high financial stress report severe anxiety.

High financial stress levels increase blood pressure, heart disease, and increase the risk of stroke by nearly 20%.

(Source: University of Nottingham & Northwestern University)

The report found that ‘fear that they won’t have enough money to last a lifetime’ is the number one concern among all demographics with almost two thirds of Americans “not confident” in their retirement and lifetime income plans, and only 27 percent confident they’ll have enough money to get them to the end of life.

[Click Here to Get Wealth Wednesdays Weekly Newsletter and Free Resources]

Demographic Divide

Confidence in a financially secure retirement seems to grow with age. 53% of Baby Boomers believe they can maintain “a good standard of living” in retirement, while just 22% of Gen Xers and 28% of Millennials shared that sentiment.

“For Millennials, it’s not surprising they aren’t confident since they’re many years away from retirement and are likely thinking more about their immediate financial needs,” says Dan Keady, TIAA’s Chief Financial Planning Strategist,

Meanwhile, A study by David C. John - deputy director of the Retirement Project and a senior fellow at the Brookings Institution - found women at-large, women of color, and minorities experience lower rates of retirement readiness than their white male counterparts.

In addition to systemic factors like discrimination, John writes financial education is a critical part to the overall financial wellness of these groups.

“Attitudes about saving are likely formed from an early age,” John writes. “Habits learned from when one is young tend to carry into adulthood. If children are encouraged at a young age to start saving and notions of budgeting are integrated into their daily lives, it may instill a positive attitude towards saving over their adult years.”

Financial Habits That Build Confidence & Reduce Stress

Keady and other financial experts agree that retirement planning should start as soon as possible, with as much money as possible.

That means if you only have a little to spare, then do it. Just starting on your retirement journey is statistically shown, according to the TIAA study, to boost confidence.

“Even just starting to think about it and putting a plan in place will greatly benefit people as they continue through their working years,” Keady said. “When individuals have no plan at all, they can feel even more overwhelmed and lack confidence.”

“People should closely evaluate their plan options and should

even ask their employer about adding lifetime income options to their plan.”

- Dan Keady, TIAA’s Chief Financial Planning Strategist

Technology has made it easier than ever to track and develop retirement savings. Apps like Acorns, Stash, and others are innovators in making investing mobile, and companies like TIAA have mobile applications to help keep retirement top-of-mind.

[Click Here To Learn About Investing In Cannabis Stocks]

Battling Uncertainty with Advice

“Two great ways of reducing uncertain outcomes are by using financial products that guarantee lifetime income and getting the advice and building the skills needed to deal with adverse events,” Fouché said.

Financial advice is best given by professionals with credentials. Certified Financial Planners (CFPs) are duty-bound by their certifications to act in their clients’ best interests, which means you can hire someone to truly have your back.

Whenever you decide that a CFP is the right choice for you, do your homework. Make sure they are certified, and can provide references to current or past clients. Not all financial planners are created equal, so it’s crucial to get the right person in your court.

When faced with uncertainty, remember that there is always a way out. Perhaps more to the point, always remember that net-worth has nothing to do with self-worth. Financial challenges do not define us - what we do about them, however, is another story.

![[Financial literacy month] 5 questions you must ask yourself about your parent’s ‘money’ role modeling](https://images.squarespace-cdn.com/content/v1/6011ce08663bad3a50903423/1619026274783-MQO949LF2AV6L2MDSO9I/Childhood+money+lessons.jpg)

[Financial literacy month] 5 questions you must ask yourself about your parent’s ‘money’ role modeling

The road to a healthy money mindset

Click Here to Listen To Stacey's Conversation With Students At Rutgers

I once interviewed a woman who was experiencing a lot of stress in her marriage about money. She and her husband were having a hard time talking about money and integrating their money – they even filed separate tax returns--but their finances had taken a turn for the worst. She realized their inability to communicate about their financial life was taking a toll on the marriage, and wanted help.

Things really came to a head when the couple was asked to disclose their assets and financial statements to a financial planner. The couple both knew that the wife had higher income – she was a lawyer, he was an artist, but her reluctance, and near refusal to share her finances were clearly being driven by something deeper.

[Starz Power Actress, Naturi Naughton, Talks Love & Money. Click Here For More!]

First impressions

The planner, who also had training in psychology and therapy, was savvy enough to start asking questions about how the couple saw their parents behave with money.

It turns out that the woman’s father would always yell at the mother, sometimes threatening violence about her spending. In order to avoid these brutal confrontations, her mother would buy things and not tell the father, hide new purchases in the car, for example, often enlisting her daughter’s help.

The child fell into the ‘hide money’ mode as an adult, and it felt perfectly natural to her. Once she became aware of this pattern, however, it no longer ran the show. She could call herself out when the feelings and tendencies surfaced. Now that she and her husband knew what was really happening, he could provide compassion and support when she needed it, and she could redirect her energy towards her true goal, which was creating the financial foundation she and her husband needed to achieve their goals.

“We simply filter information through the mechanisms we developed as a child,” says financial advisor Susan Galvan. “Those deep imprints influence every decision we make, and we use them as a reference point. If we don’t go back and look at those operating systems, we will fail. We will remain at that level of understanding if it is not revisited,” she adds.

[Click Here To Take The Wealth Wednesdays Pledge & Get Free Financial Coaching!] Lifting Each Other Up

Don’t Blame Mom & Dad

Chances are, your parents or primary caregivers didn’t realize that their unspoken words and unexamined actions were speaking volumes. And you certainly didn’t have the presence of mind to tell them, “your behavior and patterns are literally programming my brain in ways that will hurt me financially as an adult.” I definitely want to hear from you if you did!

Most important, remember that the people who raised you were dealing with their own conditioning about money from the people who raised them and the environments they were raised in. Think about that for a moment.

“This conversation is not about blaming mom and dad. It’s really about discovering the messages that you got, some recognizable and some unspoken, that have formed you now,” says Marty Carter, a family counselor specializing in financial behavior and licensed clinical social worker.

“If they’re good, you want to keep them. If not, instead of blaming mom and dad, see what you can do differently.”

A Look Inside

The point where you are bound is also the point where you will be set free. Think about the following 5 questions and see where you may need to rewrite your early scripting about money.

· What was your family’s attitude about the following: saving, spending, debt, and investing? Are their beliefs having an impact on your choices today?

· Did you see healthy discussions about money, or was there stress around money in your household when you were growing up?

· What do you admire most about your primary caregiver’s financial behavior? Why?

· What do you consider your primary caregiver’s greatest limitation when it comes to money? How do you think this has affected them?

· Imagine yourself achieving your goals. Which of your childhood money scripts would need to be re-written? What would the new messages be?

Freeing yourself

As you examine the role your childhood conditioning is playing out in your finances today, come up with 3 things you can do to step away from those early scripts and act in ways that are consistent with your goals.

For example, if you see that your early scripting has not helped you become a good saver, set up automatic deductions: have an amount that is within your budget taken out of your paycheck and automatically deposited into a savings account each month. Pick a date to start the process.

While conditioning, like those imprints we take from our role models, is powerful, it is no match for your superpowers. Instinct, intuition, the ability to change your mind, for example, are skills you were born with – skills that will light the way on your road to abundance.

![[Wealth Wednesdays] Actress Naturi Naughton of Starz ‘Power’ Talks Love and Money With Angela Yee & Stacey Tisdale](https://images.squarespace-cdn.com/content/v1/6011ce08663bad3a50903423/1618410744872-4G5GDOQOK6KCTJC4O6Z4/Naturi+N.jpg)

[Wealth Wednesdays] Actress Naturi Naughton of Starz ‘Power’ Talks Love and Money With Angela Yee & Stacey Tisdale

How Money Can Help Couples Build Stronger Relationships

By: Stacey Tisdale

Courtesy: Mind Money Media Inc.

More than 40% of couples in the United States commit financial infidelity – lying to their partners about money by doing things like hiding existing debt, excessive spending, or the amount of money they actually have.

Recently engaged, Naturi Naughton, who plays the sassy Tasha St. Patrick in Starz drama Power, recently shared with teamwealthwednesdays.com that she and her fiancé, whose name she has yet to reveal, were having none of that.

“We talk about everything, that’s one of the reasons I’m excited to marry him,” the beaming bride to be told Tisdale and Yee.

“He brought financial awareness into my life,” she adds.

[Click here to sign up for the teamwealthwednesdays.com free ‘Weekly Wealth Builder’ newsletter.]

Financial Fidelity From The Start

Naughton says she and her fiancé talked about money from the very beginning – something she says all couples should do.

“I would tell you ladies and men to say early on ‘How is your credit score? What is your financial situation.’ You need to ask these questions up front,” says Naughton.

The Power star says she and her future husband, who were introduced by her series co-star, Omari Hardwick, were not only transparent in the early days of their relationship, but they continue to teach each other a lot when it comes to financial wellness.

“I remember when we first started dating, he was very transparent,” says Naughton.

“He comes from a family that has taught him a lot about entrepreneurship, and he taught me a lot about the importance of building your own brand, doing your own thing, and being managerial,” she adds.

Lifting Each Other Up

Naughton says one of the most important things she’s learned from her fiancé is that there’s more to financial health than earning money.

“it's funny because even though I'm in the business, I was just a workaholic. You know, we think ‘if I work and I make money and I get a check, I'm good.’ But I never really went deep into those other layers of financial wellness,” says Naughton.

“There’s no one way to get money and to be successful. I think that’s important for all of us to know. We have that conversation all the time,” she adds.

What Financial Secrecy Does To Relationships

Money is a leading cause of breakups and divorce, and like most relationship problems, the culprits are usually rooted in a lack of communication and trust.

Financial infidelity is a big deal. If someone is hiding money or debt from their partner, it makes it almost impossible to make an accurate budget. In addition, if you’re keeping a financial secret, it’s only natural for your partner to wonder what other secrets you might be hiding. That’s how relationships end up in big trouble.

Despite how common it is, over a quarter of adults (27%) agree that financial infidelity is worse than physical infidelity, according to a study commissioned by creditcards.com.

The study also found that while more than a third of those who commit financial infidelity say they do it ‘for privacy and a desire to control their finances,’ almost as many say they keep money secrets because they are ‘embarrassed’ about the way they handle money.

[Blog: Click here for 5 quick tips that will help you get out of student loan debt!]

Conversation Starters

No one can deny that talking about money, particularly with someone whose opinion matters deeply to you, can feel difficult, if not impossible.

Here are some tips that will help you get these challenging conversations started:

· Communicate: Ask your prospective partner if they think it’s important for couples to be on the same page about money, and why.

· Share: Be open about your financial challenges and how they’ve impacted you financially, psychologically, and emotionally. Ask them to do the same.

· Lose the notion of right and wrong: There are no right and wrong beliefs about money, just different ones, and they all come from our individual experiences. To tell someone they’re wrong is telling them that your experiences are more valuable than theirs.

There’s a lot more to money than dollars and cents. Our sense of self, values, and belief systems all play a role in our financial behavior. While the ‘money talk’ is not easy, open communication in spite of those hard feelings will strengthen your relationship and make your bond with your partner even stronger.

Yee & Tisdale’s “Teamwealthwednesdays.com” Makes $10k Donation to HBCU, Edward Waters College

‘Dynamic Money Duo’ Determined To Make A Difference

By: Teamwealthwednesdays.com

On February 24, The Breakfast Club and Wealth Wednesdays co-host Angela Yee, and award-winning financial journalist and Wealth Wednesdays co-host Stacey Tisdale, launched a new platform called teamwealthwednesdays.com to provide resources, programming, and information to help the Black community build wealth.

Now, just three weeks later, the two are already demonstrating their commitment to their mission—with a show of support for HBCUs. They’re making a $10,000 donation to HBCU Edward Waters College. The gift was announced by Yee on The Breakfast Club Wednesday morning.

“We really need this donation,” said Aquanetta Parrot, Director of Student Activities and Leadership at Edward Waters College. “It will really do a lot for our students, their growth, and professional development.”

Click Take the Pledge to join our team and get free financial resources!

“We were moved by the number of students and alumni at the school who took the time to go to the site and take the pledge to take control of their financial lives,” says Yee.

“This is only the beginning of the ways in which we plan to provide support to institutions and individuals as we help our community build wealth through our new platform,” adds Tisdale.

Making a Difference

Prior to Covid, The American Council on Education found the HBCU endowments lag behind public and private sector non-HBCUs by at least 70%.

The murder of George Floyd and the Black Lives Matter protests that followed did garner support and raise awareness about the financial challenges HBCUs face, as well as their socioeconomic importance.

The 106 HBCUs in the United States make up only 3% of America’s colleges, yet they produce almost 20% of all African American graduates.

“Our mission and our goal is to create global leaders,” says Parrot. “We will utilize the funds from teamwealthwednesdays.com to create more resources for our students, not only focusing on wealth building, but also mental health and connecting to ensure that our students are successful all the way around.”

“Over the past month, we’ve already partnered with almost 20 HBCUs to bring them information, programming, and resources, to ensure their students are financially literate,” says Tisdale, who is also creator of the Winning Play$ financial education program, winner of the U.S. Department of Education’s Excellence in Economic Education award.

“We aim to partner with all of them in our efforts to create economic, entrepreneurial, and career opportunities for multicultural demographics in our nation,” adds Yee.

Click here to check out our Financial Wellness Center!

Join The Team

Teamwealthwednesdays.com offers educational content, programming, and resources on a range of topics including debt management, entrepreneurship, investing, homeownership, career advancement, and financial stress management for multicultural audiences.

Visitors to the site can also access free, one on one financial and credit counseling, through its partner organizations, as well as other resources that assist in credit building, preparing for homeownership, and the mortgage application process in the financial wellness center.

Visitors are also encouraged to take the Team Wealth Wednesdays Pledge to Learn, Plan, and Act, when it comes to their financial lives, and will receive a free newsletter each Wednesday with actionable advice and information that will help them build healthy relationships with money.

Wealth Wednesdays programming, social impact campaigns, and content are distributed through iHeartMedia’s The Breakfast Club.

5 Tips To Help You Manage Student Loan Debt

Moving Beyond The Challenge Of This Tremendous Financial Burden

By: Stacey Tisdale

The numbers are increasingly alarming – student loan debt is spiraling out of control. Some 45.3 million people now owe $1.7 trillion, with borrowers in debt by an average of $37,691 each. A spike in unemployment due to the coronavirus pandemic fueled the largest increase in the total student loan debt balance since 2013.

As of the first half of 2020, 11.2% of adults with student loan debt reported they were unable to make at least one student loan payment. The Cares Act, the sweeping stimulus legislation, offered some relief—suspending payments on federal student loans owned by the Department of Education from March 2020 to September 2021 and dropping interest on these loans to zero percent. This administrative forbearance did not cover private student loans.

Click Take the Pledge to join our team and get free financial resources!

Paying off student loans is wreaking havoc on borrowers’ lives. A 50-state survey created by two organizations, Summer and Student Debt Crisis, found that a vast majority of people with student debt are delaying marriage, home ownership, having children, and saving for their retirement as a result of what feels is an insurmountable debt burden.

Click here to check out our Financial Wellness Center!

Struggling with the Stress of Paying Back

In the detailed report aptly titled “Buried in Debt”, 65% of borrowers reported having less than $1,000 in the bank. A whopping 88% of borrowers say they are struggling to make their high monthly payments, with nearly two-thirds reporting their student loan bill is higher than their monthly food allowance. It’s not surprising then to learn that 86% of the borrowers surveyed in this study consider their student loan debt to be a “major source of stress.” And one in three report student loan debt was the #1 stress in their lives.

5 Tips to Help You Manage Student Loan Debt Stress

While your student loan debt is stressful, here are 5 tips to help you manage the stress – as you manage your debt.

Take action! Remember there are things you can do to lower your debt, which will lower your stress. Look at refinancing with a private bank, which can offer lower interest rates, longer payback terms, and special options like an interest rate tied to your grades.

Find alternative programs that will pay your debt for you in exchange for a commitment to work for a specific number of years. More companies are offering these programs and there are numerous public service opportunities that will reimburse college costs for a future position.

Look to see if you qualify for the Temporary Expanded Public Service Loan Forgiveness, passed by Congress in 2018. This offers debt forgiveness to a borrower who makes 120 payments over a 10-year period. Complete an application here.

Be good to yourself! Take a tip from young adults, aged 18-27, who were found to feel empowered by their student loan and credit card debt, according to a new research study. “Debt can be a good thing for young people – it can help them achieve goals that they couldn’t otherwise, like a college education,” said sociologist Dr. Rachel Dwyer of Ohio State University

Debt doesn’t make you a bad person! If the stress becomes overwhelming and the situation feels hopeless, reach out and talk to someone and explore together what options for help you might not know about.

Bottom line, a higher education is often the cornerstone of success. A college or graduate degree can open the door to a higher paying job, the salary you can make, and the goals you can achieve. But before taking on student loan debt, shop around for the best rates and payback options you can find. With private banks back in the student loan business, competition should help keep interest rates lower.

The 411 on 420: A Beginners Guide To The Marijuana Economy & Cannabis Investing

What you need to know to cash in on cannabis

By: Stacey Tisdale & Carolyn Brown

The cannabis industry is expected to triple in the next five years. There is no denying that cannabis is big business. Retail sales of medical and recreational marijuana in the U.S. eclipsed $15 billion by the end of 2020. States raked in a combined $6.9 billion in tax revenue from recreational marijuana use. Public and private cannabis companies raised $5.5 billion from investors in 2019 and $2.6 billion in the first half of 2020 amidst the coronavirus pandemic.

What makes for pot’s hot outlook? The growing number of states that have legalized cannabis in some form in recent years since California became the first to allow for is the medical use, and Washington and Colorado became the first states to legalize marijuana for recreational use.

During the 2020 election New Jersey, Arizona, South Dakota, and Montana became the newest states to legalize recreational marijuana. South Dakotans also backed creating a medical marijuana program for people with severe medical conditions. Mississippi voters approved legalizing cannabis for medical use. Virginia lawmakers recently approved legislation that would legalize recreational use of marijuana by 2024.

Just 10 years ago, marijuana was illegal across much of the United States. While federally cannabis use remains illegal, 35 states plus the District of Columbia now have laws legalizing marijuana for medicinal and/or recreational use.

Today, there are even worldwide cannabis celebrations. In cannabis culture, 420 is code for marijuana and hashish consumption, especially smoking around the time 4:20 p.m. This popular slang for smoking marijuana also comes from April 20th being an annual day of jubilee among cannabis enthusiasts.

Click here to take the pledge at teamwealthwednesdays.com and get free 1 on 1 financial coaching!

Marijuana’s Move into the Mainstream Economy

Of course, there is always backlash in any effort to decriminalize the controversial plant. But marijuana’s move into the mainstream economy is mounting. A recent survey found that 1 in 8 adults are avid marijuana users. Today, 35 states and the District of Columbia have legalized marijuana for medical use, while 15 states and the District of Columbia have made it legal for adults 21 and older to buy and consume recreational marijuana.

With President Joe Biden in the Oval Office, a Democrat-controlled House, and a 50-50 split in the Senate, there is growing optimism overseeing an end to federal marijuana prohibition. Senate Majority Leader Charles Schumer and Senators Cory Booker and Ron Wyden have announced they intend to make cannabis reform a priority this year.

According to the cannabis investment firm Viridian Capital Advisors, given an attractive growth outlook for both medical and recreational markets in the U.S., improved execution by operators, healthier balance sheets, and valuation trends for certain companies, now is an attractive time to invest in the U.S. cannabis market.

Hashing Out Cannabis Opportunities

Many top cannabis companies are expected to report positive earnings in 2021. These companies primarily breakdown into three groups. Marijuana growers and retailers that are cultivating and packaging cannabis products for consumption. Biotech firms that are developing and marketing cannabis-based drugs. Other companies that provide ancillary products and services, including consulting, distribution, hydroponics, lighting systems, and packaging.

The 13 Major Marijuana Sectors:

· Agriculture Technology

· Ancillary Cultivation & Retail

· Ancillary Products & Services

· Biotechnology

· Consulting Services

· Consumption Devices

· Cultivation & Retail

· Hemp

· Infused Products & Extracts

· Investment/M&A

· Physical Security

· Real Estate

· Software

The marijuana sector as a whole has experienced five consecutive months of moving higher in the stock market. Although there was market volatility with a sharp decline in marijuana stocks the last two weeks of trading in February 2021. Still the sector managed to see gains, with American cannabis stocks outpacing the rest of the market with 20.5% gains for the month, according to StreetInsider.com. The cannabis industry is poised to grow rapidly in 2021.

Viridian Capital Advisors forecasts more than $20 billion in cannabis sales for 2021, up from $17 billion in 2020, and expects sales to exceed $35 billion by 2025. The company anticipates economic hardship caused by COVID-19 will be a key driver of cannabis expansion in certain states with cannabis providing a rare opportunity to generate taxes and jobs.

Click here to watch our wealth building special with 50 Cent, Power’s Naturi Naughton & more!

Investing In Cannabis Stocks For As Little $5

You can get into this exploding market with just a few dollars through apps like Stash, which lets you start investing for as little as $5. Stash offers fee-free trades, fractional share investing, and account fees starting at $1 per month. Using Stash, you can invest in increments of $5 to buy single cannabis stocks. You also can opt to open an account at discount brokers such as TD Ameritrade with no minimum investment requirement.

You can purchase stock shares in companies like Green Thumb Industries (OTC:GTBIF), which has 50 operational dispensaries, but holds licenses to open as many as 96 retail stores in 12 states across the U.S. Another is Curaleaf (OTC:CURLF) which looks to be on track to become the first pot stock to surpass $1 billion in annual sales this year. Curaleaf holds licenses for more than 130 retail spots and has a presence in close to two dozen states.

Before you invest in any marijuana stock, first research the company. Examine its management team with a special focus on top executives' track records in the industry and look at the company's strategy for growth and expansion. Second, establish how much you can afford to spend. Third, check out fees, convenience, and trading platforms to determine what’s best for you.

Keep in mind the marijuana industry is still in its early stages, so many companies may not be profitable just yet. You can gauge how quickly a company expects to become profitable by checking out information that can be found in the investor relations section on company websites, annual reports, or SEC filings.

An alternative to single stock purchases is to invest in Cannabis-based Exchange Traded Funds (ETFs), using Stash or a discount broker. ETFs trade like stocks on an exchange such as Nasdaq or NYSE, but instead of buying single company shares you are investing in a basket of multiple companies.

Advantages to ETFs are trading flexibility, portfolio diversification, lower costs, and tax benefits. Want some help building an ETF portfolio? A robo-advisor might be best for you. Instead of picking your own investments, these automated online investment management services build a portfolio for you based on your goals and risk tolerance.

Stacey talks credit, homeownership, and Black wealth with Charlamagne tha God, DJ Envy, & Angela on The Breakfast Club! Click here to watch!

Using A Robo-Advisor

Robo-advisors like Wealthfront have a user-friendly platform and offer low-cost access to a diverse investment lineup, goal-setting, planning tools, banking, and a variety of tax-saving strategies. Most robo-advisors use mutual funds or ETFs rather than individual stocks to build your portfolio. They buy fractional shares, which means you could own 10 or 12 ETFs with $1,000.

What’s more, robo-advisors are much cheaper than real-life human financial advisors. Most robo-advisors charge between 0.25% and 0.50% as an annual management fee. There’s also free options like Sofi Automated Investing.